-

-

Link Copied

In a time when digitization has become standard and most daily activities and routines are processed on virtual environments, one may find it difficult to believe that such reality is a new concept. Physical boundaries no longer pose a challenge for companies, industries and consumers, with connectivity becoming the word of order and allowing interactions over land and sea. This disruptive change in social-economical behaviors has paved the way for innovation and new business models, many of them focused on cooperation to answer market demands in a quick, effective and competitive manner. This new approach is bound to affect all industries, even those which, like Banking, seemed isolated from the world around them.

In fact, Banking is pointed out as one of the most promising industries for disruptive innovation, with Fintechs and more recently Techfins such as Amazon or Google, joining the picture by acquiring banking licenses. Traditional banks must quickly adapt to new market requirements, be them imposed by law (such as PSD2) or consumers (such as new products, services and channels), who are in turn becoming increasingly demanding. To keep up with the digital transformation, banks will have to team up with Fintechs and other third-party providers, to deliver valuable products and solutions to customers, offerings they are not able to deliver on their own. Such is the concept of Open Banking.

“90% of Banks Accenture surveyed believe Open Banking will boost organic growth by 10%”

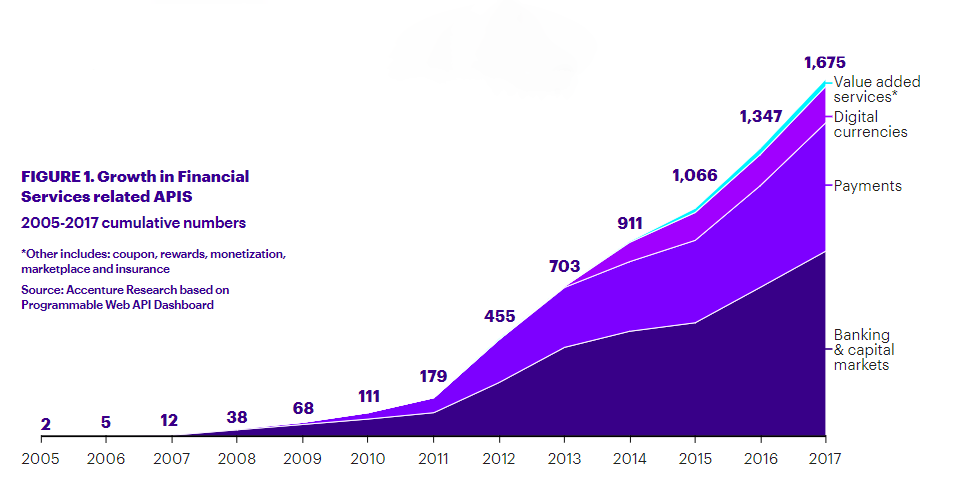

A newfound life for APIs

The rationale behind Open Banking is to deliver customers better financial products and services, by means of a safe, transparent process. By bringing together the innovative mindset, agility and digital infrastructure of Fintechs and the scale, reputation and established trust of banks, the result is a much more capable “hybrid company”. Think of it as a “collaborative model in which banking data is shared through APIs between two or more unaffiliated parties to deliver enhanced capabilities to the marketplace”, according to Mckinsey. Despite not being new to the financial industry, APIs were almost exclusively used to share information; with open banking however, new applications are being explored, namely in what regards transferring monetary balances and the delivery of financial services to both retail and business customers.

APIs are at the core of open banking: not only do they allow customers to give access to their financial data to non-bank third parties, but also allow third parties to integrate their services with those of banks to provide better offerings and customer experiences. That being said, most legacy and core banking systems are outdated or lack the capability to integrate with APIs, representing not only a hefty handicap but also a considerable monetary investment for financial institutions.

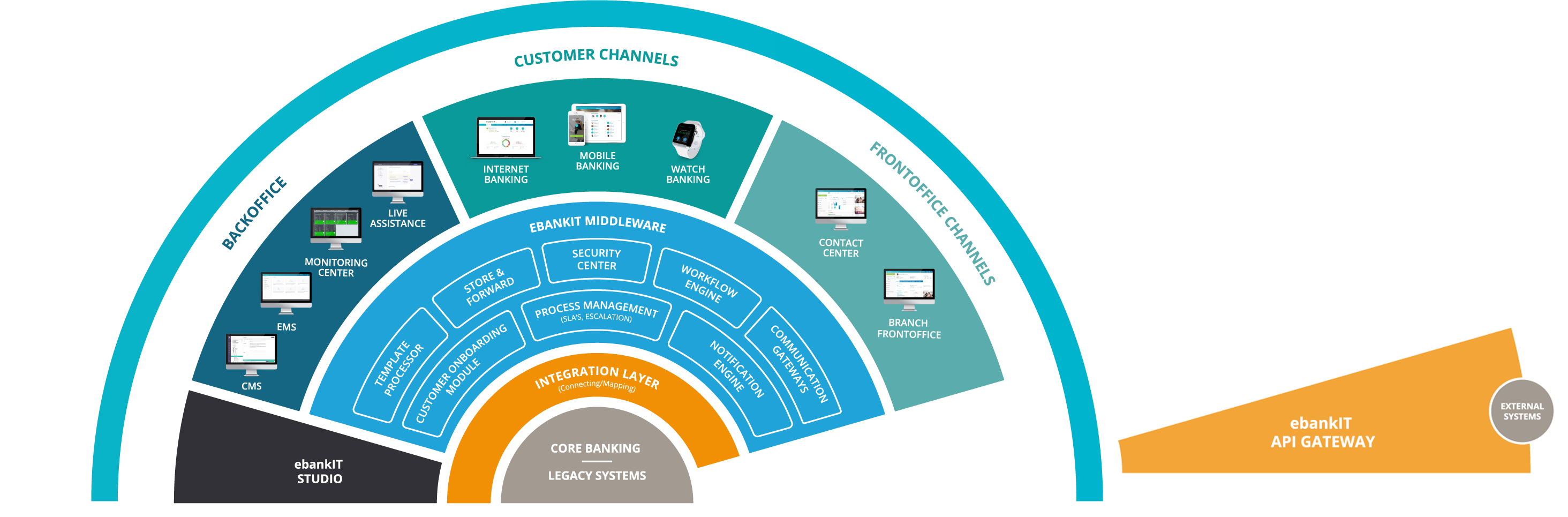

Fast and seamless integration with ebankIT

Within its several modules, the ebankIT Omnichannel Digital Banking Platform is optimized towards delivering a fast, competitive and versatile solution for banks and credit unions. One of its fundamental components is undoubtedly the API Gateway, which allows communication with External Systems and third-party APIs, thus providing banks the ability to quickly adapt to market or regulatory changes.

The ability to develop new processes and deliver new products and services with reduced time-to-market is always invaluable, but even more so in the current financial landscape where highly disruptive alterations are coming into effect:

- The EU and the UK have approved the PSD2 and Open Banking Initiative, giving more control to customer over personal account information;

- In the US major banks are leaving the aggregator model and establishing data-sharing deals with individual partners;

- In China new digital ecosystems are emerging based on data-sharing (WeChat, Alipay)

- In South Asia, Fintechs are experiencing considerable growth around APIs and data sharing

Furthermore, the API Gateway will allow integration of Partner APIs (reducing partner costs and enabling monetization) and Internal APIs (increasing operational efficiency and security).

Our Core-Agnostic Digital Banking Platform is the right choice to help you embrace Open Banking, overcome its challenges and deliver its benefits: improved customer experience, explore new revenue sources and create a sustainable service model for previously underserved markets.

%20without%20SAM%20-%20Maturity%20Level%20-%202-KO%20edit.webp?width=160&height=57&name=67768-ebankIT%20Platform%20-%20CMMI%20Development%20V2.0%20(CMMI-DEV)%20without%20SAM%20-%20Maturity%20Level%20-%202-KO%20edit.webp)